A New Era of Structured Capital

for Scaling Companies

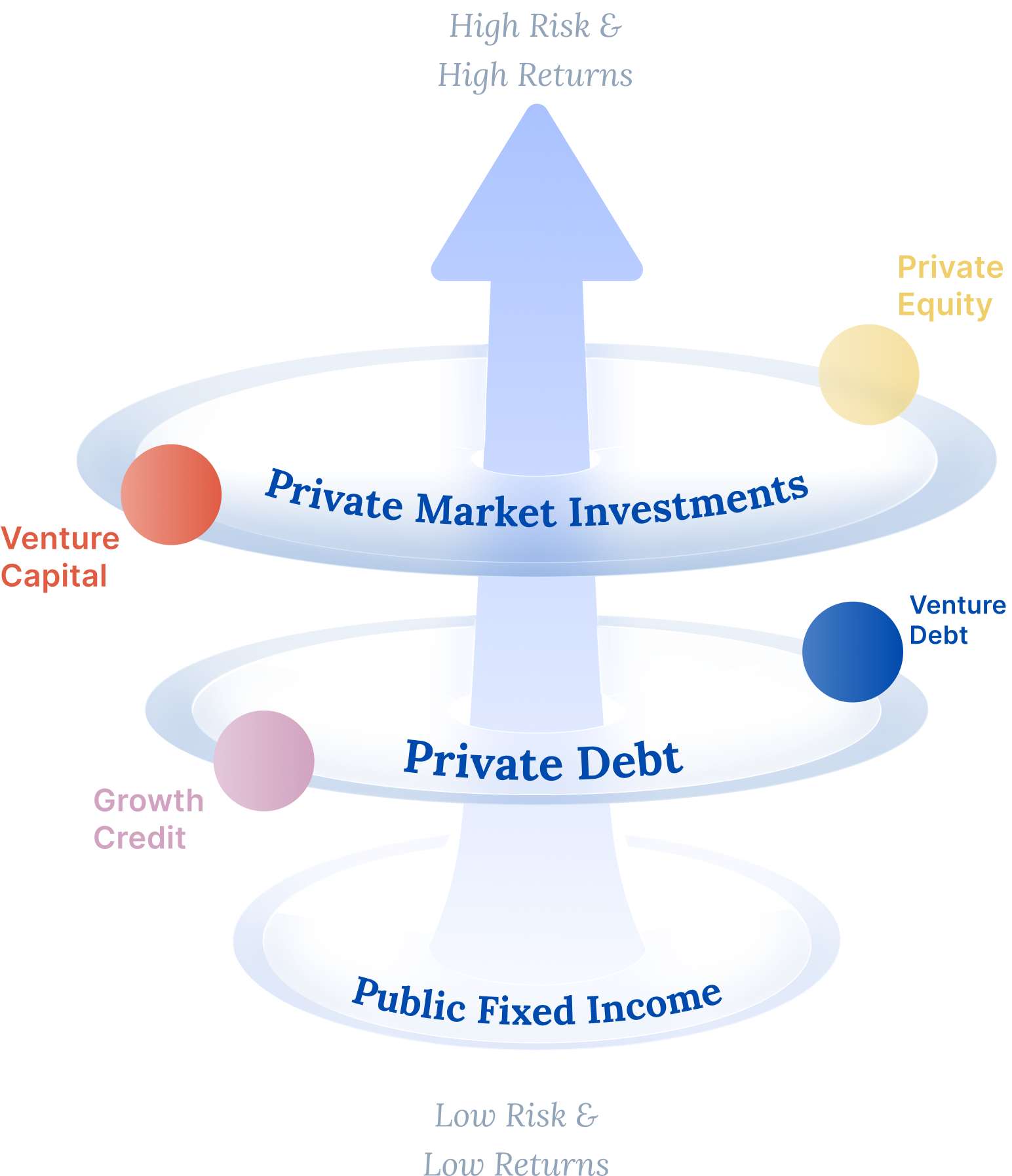

Venture Debt & Growth Credit supports companies across stages with flexible capital, combining growth ambition with disciplined risk and structured financing.

Private debt has evolved into a key pillar of modern financing, adapting to companies’ needs as they scale. Venture Debt supports earlier-stage, venture-backed businesses focused on growth, while Growth Credit enables larger, scaled companies, backed by institutional investors - to access capital with greater emphasis on stability and structured expansion. The Global Private Debt Report 2026: A Venture & Growth Credit Lens captures this shift across the maturity spectrum, highlighting how these segments together are shaping a more disciplined, multi-instrument approach to growth financing.